-

Japan: Tokyo

Vietnam: Hanoi & Ho Chi Minh

-

(81) 3 5829 4006

(84) 24 3978 5165

By: B&Company Vietnam

Industry Reviews

Comments: No Comments.

Technology-based Personal Finance Solution is a rising trend in the dynamic fintech market in Vietnam. From nearly 400.mil USD market value in 2017, it expects to have a CAGR of 31,2% during the period 2017 – 2025 to reach 24% of total fintech market share in 2025, according to a report by consulting firm Solidiance.

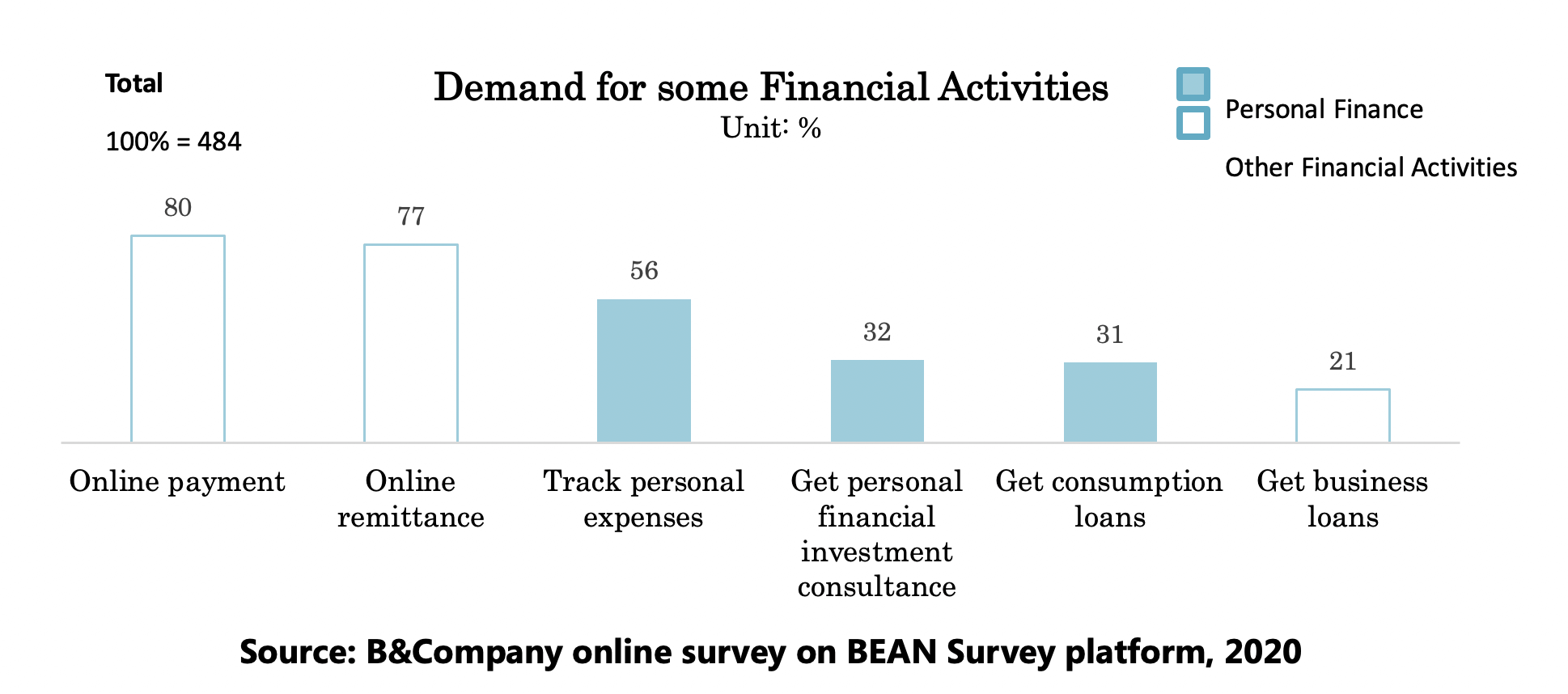

A survey conducted in May 2020 by B&Company on its online survey platform BEAN Survey with 484 respondents above 18 y.o shows that demand for Personal Finance activities are significant with 56% of respondents wanting to track and manage their expenses. Respondents also shared desire to get advice on personal finance investment (32%) and obtain loans for consumption purposes (31%).

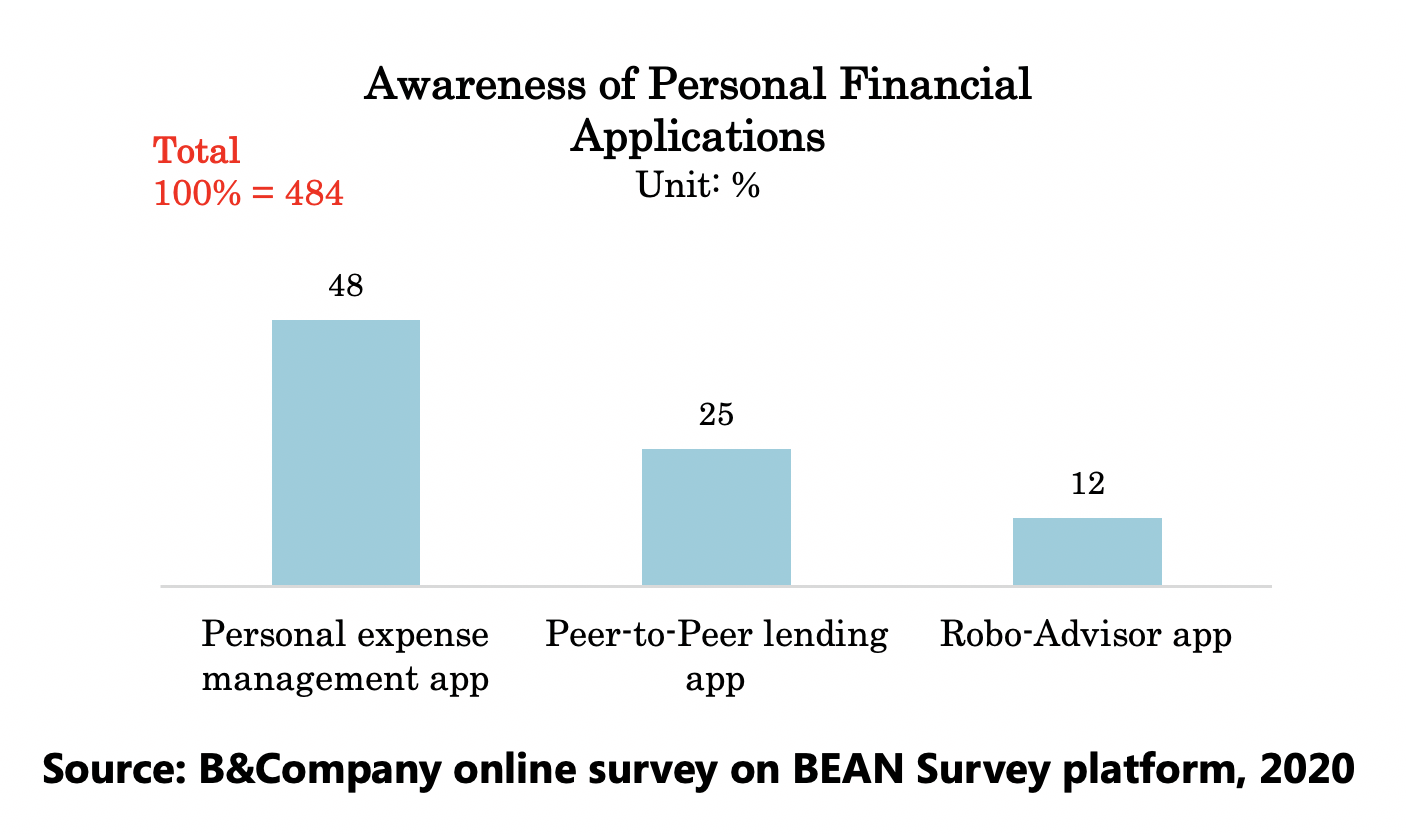

Responding to the potentials, Personal Finance Applications including Peer-to-Peer (P2P) lending platforms for individuals, personal investment apps using artificial intelligence (Robo-advisor), and Personal Expense Management Applications have appeared in Vietnam in the past few years. B&Company survey results also indicate that a considerable proportion of respondents are being aware of Personal Finance Applications, the leading position belongs to personal expense management apps. Social media is the most common channel where people get to know Personal Finance Applications.

The list of most awarded applications to Vietnamese users for Personal Expense Management is comprised of both domestic and foreign players.

According to the survey result, Money Keeper – So thu chi Misa, a product by Misa JSC, a well-known accounting and management software company in Vietnam, is the most popular. Another domestic player, Money Lover of Finsify, is expected to be a promising opponent in this market, with its rank as the number one Android mobile app in Personal Finance solution, by Google’s announcement in May 2017.

The survey also points out one big challenge for these apps is how to drive consumers’ habits and become more attractive to prospective customers. Many respondents who track expenses prefer using other alternatives, such as tracking expenses on e-wallet (75%) or on banks’ applications (67%). 43% of respondents who know but do not use expense management applications have said that they are curious but not yet see any clear benefits to start using. Current app users consider many app-selecting factors such as information security (76%), fees (59%), app’s processing speed (61%), features (60%) and interface (49%), and language used in the app which makes foreign apps less advantaged than Vietnamese ones (41%).

P2P Lending apps emerged with strong potential in Vietnam consumer lending landscape but is under closure consideration due to Government regulation

The second most popular type of Personal Finance Application, according to B&Company survey, is P2P lending. The ease to access small-size consumer loans through P2P lending applications without complicated requirements and procedure is expected to be a big help for people, especially for the unbanked, which is about 37% of Vietnamese adults as of 2018, according to the State Bank data.

Emerged since 3 years ago, there are now around 40 companies claiming to provide P2P lending service in Vietnam, including individual-to-individual lending and individual-to-business lending. B&Company survey shows that some most popular individual-to-individual P2P applications are Vietnamese-made including MoneyBank, Vaymuon, Tima, Interloan, and Finn.

However, P2P lending service is not fully regulated in Vietnam since the legal framework for P2P lending is still under development by the State Bank of Vietnam. Recently, the companies in the field usually register as investment consultancy firms instead of financial institutions. In some cases, the companies which claim itself as P2P lending charge exorbitant interest rates, high uninformed fees, or resort to threatening tactics, harassment, and even violence to recover loans, which is considered as black credit. These downsides make the market look misleading and consumers may feel aversion to online lending applications. The B&Company survey result indicates that the reason for 67% of respondents who know but not use P2P lending apps is due to the fear of black credit impersonating P2P lending.

It is expected that the Decree on the experimental mechanism for controlling financial technology activities in the banking sector will be submitted to the Government for approval by the State Bank within 2020, and most likely from 2021, Vietnam will officially approve for some banks and Fintech companies to pilot providing P2P lending activities, which will lift the sector to a new development stage.

Robo-advisor solutions are relatively new, requiring more time and effort to acquire customers’ trust

The least popular type of Personal Finance Application in B&Company survey is Robo-advisor. In developed financial markets such as the USA, Germany, and Singapore, Robo-advisory has become a money-burning race with the participation of start-ups, brokers, asset management companies and insurance companies. But that is not the case for Vietnam, where the concept is still fairly new to consumers, and only witness a few pioneering players.

In May 2017, Techcom Securities (TCBS), a subsidiary of Techcombank, became the first company to bring Robo Advisor named TCWealth to the Vietnam market. In the same year, start-up Finhay launched its application that allows customers to start personal investment activities with just as little money as $2. Finhay has successfully raised capital from both domestic and foreign investors, and soon become one of the Top 100 Fintech companies in the world in 2019, according to a KPMG report.

IRA of Tan Viet Securities JSC (TVSI) and iBroker of BIDV Securities (BSC), a subsidiary of BIDV, recently joined the market in 2019 but seem to be catching up in term of market awareness, based on the survey result.

Despite being new, Robo-advisor applications could be very potential as the demand for personal investment advice is relatively high. However, the current market lacks appropriate service supply.

Furthemore, following B&Company survey results, user acquisition will not be easy as Vietnamese people do not have high trust in the effectiveness of automatic advice, especially when considering the characteristics of the Vietnam financial market, customers are also worried about fraud and information insecurity.

To take an overall forward view, even though each type of Personal Finance Applications would face typical challenges, the Personal Finance segment still expect a promising growth thanks to many facilitating factors such as peoples’ significant need for Personal Finance activities, high internet penetration rate and smartphone usage through which people can approach fintech products via social media, websites, etc, and the Government’s policy orientation towards a safe and secure fintech environment for fintech companies to grow as well as protecting rights of users.

Hai Ngo

Reference:

- https://www.sbv.gov.vn/webcenter/portal/m/menu/trangchu/ttsk/ttsk_chitiet?leftWidth=0%25&showFooter=false&showHeader=false&dDocName=SBV400281&rightWidth=0%25¢erWidth=100%25&_afrLoop=7500037377906211#%40%3F_afrLoop%3D7500037377906211%26centerWidth%3D100%2525%26dDocName%3DSBV400281%26leftWidth%3D0%2525%26rightWidth%3D0%2525%26showFooter%3Dfalse%26showHeader%3Dfalse%26_adf.ctrl-state%3Dohle8g3gr_1158

- https://www.solidiance.com/insights/others/infographics/disruption-by-fintech-transforming-vietnams-financial-services-ecosystem-1

- http://hca.org.vn/userfiles/files/Tham%20luan%20VIO%202019/06_Slide_Fintech_10_2019_English_final.pdf

- https://www.mbs.com.vn/uploads/files/Bao-cao-IB/1_-Vietnam-fintech-report_22102018.pdf

- https://www.allens.com.au/globalassets/pdfs/insights/asia/peer-to-peer-lending-in-vietnam.pdf

- https://bvsc.com.vn/NewsTools/Print.aspx?newsid=732559

- https://vietcetera.com/en/money-lover-a-vietnamese-built-fintech-mobile-app-going-global/

- https://english.vietnamnet.vn/fms/business/196765/peer-to-peer-lending-increasingly-popular-in-vietnam.html

- http://tapchitaichinh.vn/ngan-hang/nhieu-rui-ro-voi-cho-vay-ngang-hang-316916.html

- https://cafef.vn/du-kien-nam-2021-se-cho-thu-nghiem-fintech-trong-do-co-p2p-lending-2020060209381798.chn

- https://tinnhanhchungkhoan.vn/fin-tech/dich-vu-robo-advisor-danh-chiem-thi-phan-tu-van-tai-chinh-truyen-thong-273072.html

- https://forbesvietnam.com.vn/tin-cap-nhat/ung-dung-tai-chinh-finhay-nhan-dau-tu-tu-nguoi-dong-sang-lap-acorns-10122.html